I’ve been asking visitors to my college blog and Facebook page this week to send me questions regarding the Free Application for Federal Student Aid and the CSS/Financial Aid PROFILE.

I am sharing some of their questions and my answers today because I know other people are just as puzzled about aspects of these two financial aid applications.

If you have a financial aid question, please use the comment box below or head over to my Facebook page and ask there.

Question:

Please list any benefits to filling out the FASFA if a family’s expected family contribution is very high.

Answer:

If your EFC is very high, the reason to file would be to gain access to federal college loans. The federal Stafford Loan is only available to students who complete the FAFSA. A child also can’t get a work-study job on campus without completing the FAFSA.

What’s more, if a student applies to a very expensive school, a wealthy child might still qualify for need-based aid if the EFC is lower than the cost of attendance. And wealthy families can sometimes qualify for need-based aid if more than one child is in college simultaneously. That’s because your Expected Family Contribution for each child will drop roughly 50% via the FAFSA methodology and about 30% for the PROFILE methodology.

Question:

My ex and I were supposed to be divorced by Dec. 31. Long story short, the judge didn’t sign the papers by the end of the year. So now I have to file as married filing separately, which will go to the FASFA. The ex won’t be assisting with college tuition. Will colleges still require that his tax return be part of the FASFA?

Answer:

Your marital status on the last day of 2012 won’t matter. You will be asked to state your marital status as of the day that you submit the FAFSA in 2013. Check out my previous post on divorce and financial aid: Divorce and Financial Aid.

Question:

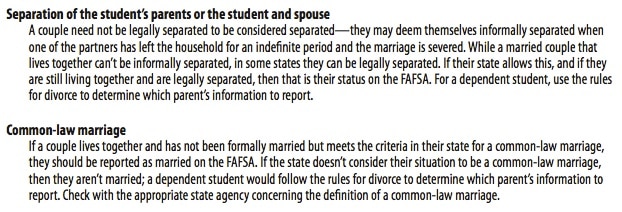

How is a separated couple treated for financial aid purposes?

Answer:

When completing the FAFSA, separated couples should use the rules applying to divorced. Here is what the federal government says about separated couples and common-law couples:

Question:

We saved and saved and actually have $ for our child to go to the public school he was accepted to and the money is in our name. Is it worth filling out the FAFSA so he can get merit scholarships etc??

Answer:

I don’t know of a single college or university that requires filing the FAFSA to qualify for merit money, but that doesn’t mean there aren’t any. Just to be safe, I would ask the state university if merit scholarships are available without filing the FAFSA.

Question:

If I am considered to be a dislocated worker on the FAFSA, do I have to provide proof.

Answer:

No you aren’t required to verify that you are a dislocated worker, which generally means that you were working, but are now unemployed. Not everyone who is receiving unemployment checks can be considered a dislocated worker. Typically those who quit their jobs are not considered dislocated workers, even if they do collect unemployment checks.

Lynn O’Shaughnessy is the author of The College Solution: A Guide for Everyone Looking for the Right School at the Right Price.

Lynn O’Shaughnessy is the author of The College Solution: A Guide for Everyone Looking for the Right School at the Right Price.

Just completed FAFSA, my EFC is high and I am displaced or unemployed. Had a great job but would not have been able to contribute what this FAFSA program says that I can. The program is written for typical situations, there is no room for ‘real life circumstances’ as many others mention above. So we get to contact the school(s) and request an appeal. Should have never been employed to begin with, then kids education would have been free.

Yes you are doing the right thing to appeal to the school. It’s called a professional judgement. You are very wrong to think that if you had never worked your child would have gotten a free education. That very, very rarely happens.

Lynn O’Shaughnessy

Hi Lynn,

Our family is in a unique situation here. My son is a US citizen, but we, his parents, aren’t. We have been living outside of USA for many years, and he’s homeschooled. This financial aid exploration is very much an unfamiliar territory for us. How will our family context affect filling out the FAFSA and calculating our EFC, as it requires US-related income, & tax records? Will this naturally disqualifies him from filling out the FAFSA, or put the EFC figures to our disadvantage? thank you.

Hi Lynn,

My child was accepted into an Ivy league school. My EFC is 5K. I am 57 yrs old.

My sole prop went out of business this year. I have no income. I own the building and plan on renting it out to another business. The rent would be my only source of income around 50K annual. No one willing to hire 57 year old man.

My building worth 1M. The ivy school is counting the building as an asset. Wants me to pay 50K for tuition per year. How can this be accurate? I need the building to generate 50K annual income. School wants all my income. Doesn’t seem to understand or care if I can eat.

I Cant get a loan because rent is my only source of income. Family expenses are 50K year.

School has no empathy for kid that earned own way into IVY league.

Kid cant go and they don’t care.

I am approaching retirement age with eight years of college coming up. I currently contribute to a self-employed retirement account, and I understand that those contributions will be added back as “untaxed income,” and so will affect EFC. Now suppose I make a withdrawal five years from now when I am retired. Am I correct in assuming that the withdrawal will also count towards EFC? I imagine $5K going into the account this year, coming out in five years and counting twice toward EFC. Seems like double taxation.

FAFSA question about assets. My husband and I own a cabin in the woods that is not rentable but I suspected it is hurting our financial aid. ( We make about $70K and had an EFC of 17500.) This hunting cabin is worth about $60,000. I am on the fence about keeping this property. I am thinking of selling it and buying a small apartment for rental income, thereby turning this property into something other than a liability.

FYI: From your column I see that I can not allow my daughter to accept the $72,000 merit scholarship that she received to attend a LAC which would still leave her with an obscene amount of debit…at least the same as the merit scholarship if not more. She is talking a gap year next year so we have time to learn more from you!

Hello Lyn, came across you info. and I am so glad. I have 2 child. attending NYS Communty Collg. I live in Suburb. NYS. come Sept 2013 they’ll both want to transf. to 4 yr. State Un. or a city Coll. in NYC. We have applied for FASFA and received awards for past 2 yrs. My gross incm. is mid 60’s. Q. aside from the FASFA aid which will probably increase as per cost increase, what other type of loans shoud I look into to to cover the rest of tuition and dorming? Will the stafford loan be enough? do schools also offer a loan option? aside from work study? and if they want to live off campus, will a private bank-student loan allow to pay for off campus rent? or will I be responsible for that off campus cost? any info and more is greatly appreciated…..worried and frustrated parent…..Thank you

My wife and I purchased my father-in-laws house in 2005 to alleviate him of the burden of maintenance etc. This is a second property that we do not live in. The town has the valuation at about $220,000. I had an informal “Market Analysis” done by a real estate agent in 2012 and the valuation came in at $105,000. I still owe $185,000 on the mortgage. My question is where the FAFSA or Profile ask for the value of real estate other that the primary residence, can I put down what my best guess is or do I go with the town valuation? Do I need to get an appraisal? Based on recent home sales in the neighborhood, I would guess my valuation is somewhere around $150,000.

Thank you for all of the great information!

Hi Richard,

You don’t need an appraisal. You can base it on home sales in the area or you can look at what Zillow values it at.

Lynn O’Shaughnessy

Lyn, similar to your question above (and copied below), if we have an EFC of $99,999 and therefore will not qualify for any need-based aid, do we need to fill out the CSS Profile (for those schools that request it) before any merit aid is released?

Question:

We saved and saved and actually have $ for our child to go to the public school he was accepted to and the money is in our name. Is it worth filling out the FAFSA so he can get merit scholarships etc??

Answer:

I don’t know of a single college or university that requires filing the FAFSA to qualify for merit money, but that doesn’t mean there aren’t any. Just to be safe, I would ask the state university if merit scholarships are available without filing the FAFSA.

When figuring financial aid awards, do schools look at need or merit aid first? Because of client payment problems, our family income is $20,000 less this year than last year, so it could be $40,000 more next year, including the late payments we should have received this year. Merit awards usually seem to be extended for all four years, and need-based awards on an annual income-based basis. If our income takes a big jump next year, any need-based aid would be reduced significantly for next year. In that case, we’d be wishing we’d chosen the school with a bigger merit award.

With an AGI of $120K this year, we do not qualify for federal money. I find myself in the odd position of wondering whether my daughter might get more aid over the four years if we had a higher income this year. Any thoughts?

Thanks for your time.

Lynn,

If my son will be in graduate school and my daughter will be a freshman can I claim two dependents in college on financial aid forms. I see conflicting information on this question on the web and on school net price calculators.

Thanks.

Graduate students are independent students so it’s my understanding that you can’t claim the graduate student, who can after all receive greater federal aid because of his status as independent.

Maybe some private schools that use the PROFILE might give a break to a family through a professional judgement. I would ask this question of the schools your daughter is applying to.

Good luck.

Lynn O’Shaughnessy

Stuart,

Lynn is correct that students who already have their 1st bachelor’s degree, are indeed considered “independent” students. Strangely though, some graduate schools twist the rules to still require that those “independent” students provide parental info (think business schools, medical schools, etc.)… so with that line of thinking, it may be to your benefit to ask graduate schools that require that info (if your son is applying to any of those), to consider the family’s number in college to include both grad and undergrad students.

That being said, I have not seen schools give families the benefit of “more in college” when talking about graduate students and/or one of the parents going back to school.

Be prepared to fill out the FAFSA for one in college, in your example above.

Great advice Todd. Thanks!

Lynn O’Shaughnessy

Hi Lynn,

Here is my FAFSA question: My son applied Early Action to some colleges and he has been accepted to two that also gave him merit aid and music scholarships. I’ll use general numbers to make my point.

Most of the colleges he applied to cost around $50K

My EFC usually comes up around $40K

The merit aid he has been offered is about $15K, bringing the pre-FAFSA cost down to $35K

When I apply for FAFSA, my need should be about $10K

Will the colleges that meet a high percentage of need consider that $10K? Or will they say “we already gave this student $15K, so there’s no need”?

Would he still be offered work-study? Does everyone who want that option get it?

Thank you.

Hi Denise,

Because your EFC is $40,000 and your son already received merit aid of about $15,000 for these schools that cost around $50,000, you couldn’t expect anymore money from the schools. Your son’s merit aid covered the gap between your EFC of $40,000 and the cost of the school – around $50,000.

Your son could look on the schools’ websites to see if they offer any additional talent scholarships that require a separate application. Plenty of schools offer these and few students know about them. You can also find merit scholarships for individual schools at MeritAid.com.

Good luck.

Lynn O’Shaughnessy